What Good MI looks like

In short, it's quality information that allows you to make informed management decisions to improve the profitability and value of your business. Good implies that it meets your individual requirements, it’s sufficiently detailed but not too much and that you fully understand it – you own it. But it needs to be prompt – another ingredient of Good. It needs to tick all these boxes to be successful.

Good does not mean it needs to be voluminous. Every user is different. Some will really benefit from 40 pages, others will do much better with 4. Some love bar charts, some hate them - of course both can be provided. It's really up to you as an individual to work it out and then make your requirements known to whoever is producing the MI. They are your accounts – not those of the accounts producer. There’s nothing wrong in taking advice on what is Good – not every user is financially skilled. There is nothing to stop you being guided by someone who has the expertise, so that you're in a position to understand and benefit from the Good MI.

Good implies that the information is sound. It's not Good if it’s beautifully produced and prompt but not reconciled or wrong. So it’s crucial to take whatever steps are necessary to ensure that it is sound. This may include a quality Health Check. This is not difficult to organise - it’s just a matter of asking.

An average user would list the following as possibly known information:

• sales

• sales orders

• what’s in the bank or not

What most users would not know, which Good MI would provide, is:

• a cash flow forecast for some months – to avoid problems

• the gross margin percentage – so it’s measured then improved

• the overheads costs – so it’s measured and then reduced

• a quality Profit & Loss with comparison to budget / previous year – so profitability is boosted

Notice a pattern here? Measure the things that matter then you can determine what action you want to take and track progress. Do this and you are in control of your business performance. You are not just letting it happen or, even worse, not even knowing what has happened.

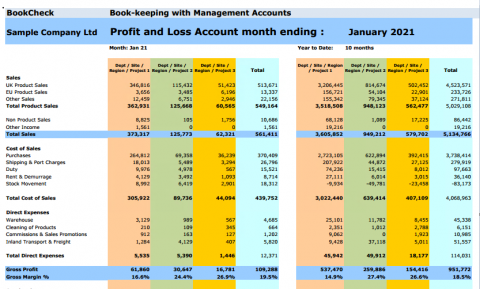

A Good system includes management accounts that are of the quality of the year-end but tailored to your specific information requirements and produced soon after each month end. Some businesses have it, most don’t. Of course these reports need to include the gross margin % - much better when split between different sectors of the business. For instance, in BookCheck there are in effect two businesses. The first is bookkeeping with management accounts and the second is payroll with the auto-enrolment. They are really separate businesses which is why we produce their own P&L reports each month. Not surprisingly they produce different margin percentages. Then when the margin changes we know which side has caused it. Otherwise it would be pure guesswork, which is worse than useless.

What it can do for your Business

The most important objective in your business is to ensure that you don't go bust or run into serious cash flow difficulties. So Good MI in the form of a cash flow forecast is a vital part of preventing such a disaster. This is particularly necessary in current times when businesses are regrouping after the pandemic. Many are growing rapidly, compared with say a year ago. Counter-intuitively this is a potentially dangerous situation because it's likely that such growth will cause a cash flow issue or crisis. Will there be sufficient receipts at the required time to pay the bills and your staff? It's absolutely critical that this is considered.

The second most important objective is to make as much profit as possible. That is somewhat different to increasing sales, which is the automatic urge. Increasing sales is all very well, as long as the focus is on profit. This of course assumes you know what the profit margin is of each project/contract or product or service – do you have this information? This is where Good MI really scores. Fixing this gap will probably be the most profitable step you could take.

There is a massive almost hidden benefit of Good MI which is not to be undervalued. It takes an enormous amount of pressure off management if the facts are known. Informed decisions can then be taken to improve. Otherwise it’s stressful trying to work out what to do which tends to result in an undue focus on increasing sales.

It's really important to understand the effect on profits of changes to the selling prices, both up and down. In chasing sales it's very easy to assume that a reduction of say 10% in the selling price is going to be a good idea, because it will increase sales by more than 10%. This is horribly wrong as this example will show. Suppose your gross margin is 40%

| sale units | sale £ change | sale each | cost each | profit each | profit total |

| 100 | £10 | £6 | £4 | £400 | |

| 133 | -10% | £9 | £6 | £3 | £400 |

| 80 | 10% | £11 | £6 | £5 | £400 |

With a 10% reduction in selling price you would need no less than 33% more units of sale, just to stand still. Not attractive. On the other hand, increase your price by 10% and volume can drop by 20% - far more attractive. Find your margin and play with the numbers. It surprises just about everybody.

An associated challenge with a lot of MI is that it involves serious time from a director level or even an expensive FD in its production. This is a questionable use of such valuable time. With poor quality MI it's a double whammy. Good MI scores a double bonus here.

All in all an impressive list of the real benefits of Good MI – achievable by every business. If you would like to talk to us to see how we can help put Good MI in place for your business and put you on the road to better performance, please get in touch.